Digital Identity and Fake Credit: New Fraud Schemes

Online fraud has come a long way from stolen credit cards. Today, the game has changed. Criminals are creating fake people from scratch — not impersonating you, but inventing someone new with your details. It’s called synthetic identity fraud, and it’s now the fastest-growing form of financial crime. Powered by a mix of stolen data and digital tools, these fake identities are opening credit lines, taking out loans, and leaving banks — and sometimes real people — to deal with the fallout.

As digital systems expand, so does their vulnerability. Lenders are under pressure to move fast, approve quickly, and serve remote applicants — all of which give synthetic fraudsters an opening. They don’t just hack accounts anymore. They build identities that pass every check — until the day the credit disappears.

How Synthetic Identity Fraud Actually Works

It’s Not Just Theft — It’s Creation

Traditional identity theft relies on stealing everything from a real person — name, number, card, address. Synthetic identity fraud is more advanced. It uses a combination of real and fake details to build a new identity. Think of it like Frankenstein: a real Social Security number from a child, a fake name, a made-up job, and a working phone number. The result is a person who doesn’t exist, but looks very real in the system.

What Goes Into a Synthetic Profile?

| Element | Used For |

|---|---|

| Stolen SSN | Links to a real record, usually a minor or unused ID |

| Fake name | Prevents duplication or matching with known victims |

| False address | Used to create fake utility bills or credit files |

| Fictitious employer | Used for income and job verification |

| Real phone or email | Receives calls and passes basic ID checks |

Fraudsters take their time. They apply for small credit lines first, make a few payments, build a score — and only then request larger loans or cards. When they vanish, there’s no one to track down. And since the identity was synthetic, the real person whose SSN was used may never know.

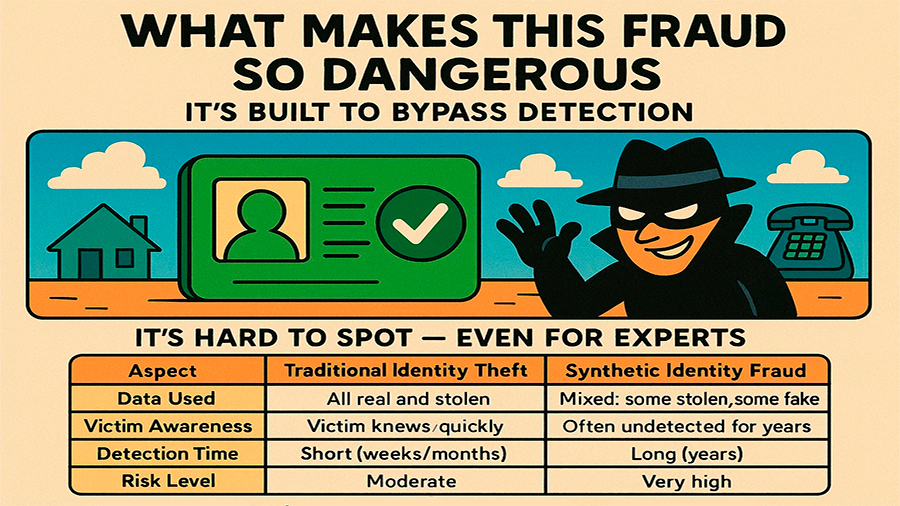

What Makes This Fraud So Dangerous

It’s Built to Bypass Detection

Synthetic identities are designed to look legit. Credit bureaus might not flag them because they don’t match known fraud patterns. Lenders often use automated approval tools that verify surface-level data — name, address, ID, and phone number. If those line up, the green light comes through. And that’s exactly what fraudsters exploit.

It’s Hard to Spot — Even for Experts

| Aspect | Traditional Identity Theft | Synthetic Identity Fraud |

|---|---|---|

| Data Used | All real and stolen | Mixed: some stolen, some fake |

| Victim Awareness | Victim knows quickly | Often undetected for years |

| Detection Time | Short (weeks/months) | Long (years) |

| Risk Level | Moderate | Very high |

The real threat isn’t just the money lost — it’s the scale. These schemes can run hundreds of synthetic applications at once. Some estimates suggest that up to 5% of “bad debt” in lender portfolios is actually synthetic fraud. That’s billions in unrecoverable credit across banks, credit unions, and fintech lenders.

Deepfakes, AI, and Fraud on Steroids

Fake Faces and Voices Are Here

Fraud has always adapted with technology. Now, with deepfake tools and generative AI, fraudsters can give their fake profiles a face — literally. AI-generated selfies are used to pass video verifications. Synthetic voices, built from samples, are used in phone-based identity checks. It’s not science fiction. It’s happening now.

In some cases, fraudsters create LinkedIn pages, job websites, even full employment histories — all fake. This helps pass more rigorous lender checks, especially for high-value applications. If the system relies on automated screening, a synthetic borrower can look perfect.

Warning Signs for Lenders and Users

Fraud Leaves a Trail — If You Know Where to Look

Even the smartest synthetic profiles have cracks. Spotting those cracks early is key. Here’s what to watch for:

| Red Flag | Why It Matters |

|---|---|

| No credit history, high loan request | New identity trying to leap straight to big credit |

| SSN recently issued | Often tied to fabricated identities |

| Inconsistent documents | Multiple mismatches suggest falsification |

| Same IP for multiple applications | Fraud rings often use shared devices |

| Free email domains or burner phones | Common among synthetic profiles |

No single flag confirms fraud, but patterns matter. When systems cross-check multiple data points — IP, behavior, document metadata — the cracks begin to show.

Why It Matters for Real People

Synthetic Fraud Can Still Hurt You

Even if the fraud isn’t in your name, your data may be part of it. Children are frequent targets because their SSNs are clean and unused. Many parents only find out when their child is denied student loans years later. And sometimes, the same phone or address is linked to both your real file and a synthetic one — confusing your records and complicating future credit applications.

False Links, False Denials

People whose information overlaps with a synthetic identity may get flagged as high-risk. Applications can be denied. Rates can go up. Or worse, your own credit file may show accounts you never opened — but that aren’t considered identity theft because technically, they’re not “you.”

What Can Be Done?

Banks and Lenders Need Better Tools

Fighting synthetic fraud means moving beyond name and number matching. Lenders now use advanced tools like device fingerprinting, behavior analysis, and real-time ID verification with liveness detection. But adoption isn’t uniform. Smaller lenders and quick-approval marketplaces are still vulnerable.

Credit Bureaus Are Playing Catch-Up

Credit agencies are developing systems to spot synthetic files early — for example, by flagging Social Security numbers that belong to minors or that show inconsistent use patterns. Some offer synthetic ID alerts to institutions, but consumer awareness is still low.

What You Can Do

- Monitor your credit reports for unknown accounts or aliases

- Freeze your child’s credit if they don’t need it

- Never share your ID details with unknown lenders or websites

- Report any suspicious accounts tied to your name or address

The Bottom Line

Synthetic identity fraud isn’t about stealing what’s yours — it’s about building something fake from the pieces. That makes it harder to spot, harder to stop, and more dangerous in the long run. Banks lose billions. Victims lose time. And sometimes, people don’t even know they’re affected. As deepfake tools and AI evolve, these schemes will only become more convincing. Fighting back means knowing the signs, demanding stronger checks, and protecting your identity before someone else builds a fake one with it.