What Rights a Borrower Has in Case of Problems with Payments

It’s one thing to take out a loan when everything is going well. It’s a whole different story when life takes a turn — your job ends, bills pile up, and suddenly, that monthly loan payment looks impossible. Most people freeze or panic. But here’s the truth: you have more rights than you think. Missing a payment doesn’t make you powerless. There are systems, protections, and options designed exactly for moments like these. If you know how to use them, you can avoid the worst-case scenarios — like default, legal action, or long-term damage to your credit.

You Have the Right to Ask for Help — Immediately

Lenders Prefer a Conversation Over Silence

Most lenders don’t want you to default. It costs them time, money, and often leads to losses. That’s why the very first thing you should do when you anticipate payment trouble — not after you’ve already missed one — is call or write your lender. Explain the situation. Job loss? Illness? Unexpected expenses? The earlier you reach out, the more options they may be able to offer, especially if your loan is still in good standing.

Hardship Programs and Temporary Adjustments

Many lenders have internal hardship programs that aren’t advertised. These can include payment deferrals, interest-only periods, temporary rate reductions, or adjusted due dates. You have the right to request these, and they must disclose what’s available under the law. In some countries, financial institutions are required to assess your situation fairly and provide alternatives when possible — not just say “no.”

Your Contract Might Already Include Flexibility

Grace Periods and Built-In Clauses

Loan agreements often include grace periods or specific terms that apply during financial hardship. For example, some personal loans allow one skipped payment per year without penalties. Mortgage contracts might have forbearance provisions triggered by income loss. These clauses are easy to miss unless you read the fine print, but they’re there — and they’re enforceable.

Restructuring Isn’t Defaulting

If you can’t make the agreed payments, restructuring the loan is an option — not a failure. This means you may be able to stretch the repayment term to reduce monthly costs, or temporarily switch to interest-only payments. Your credit score won’t take a hit just because you asked. In fact, being proactive often protects your credit more than struggling in silence.

Legal Protections Exist — Use Them

Consumer Protection Laws Work in Your Favor

In many jurisdictions, borrowers have a legal right to be treated fairly, especially when experiencing hardship. Lenders must provide clear notices before taking legal action. In the EU, for example, consumers are protected from aggressive collection tactics and unfair terms under the Consumer Credit Directive. In the US, the Fair Debt Collection Practices Act prevents harassment or misleading threats from collectors. Know your country’s laws — they’re often more powerful than you think.

Right to Transparent Communication

You’re entitled to know exactly what you owe, what fees are being charged, and what your options are. If your lender won’t give this in writing, that’s a red flag. Keep records of all calls, emails, and documents. If things go wrong, having a paper trail will help you if you need to escalate to an ombudsman, regulatory agency, or legal advisor.

Options That Can Stop the Bleeding

Loan Forbearance and Deferment

Forbearance is a pause in payments. Deferment can sometimes stop interest from accumulating. These tools exist for student loans, mortgages, and increasingly for personal loans. You have to apply — and qualify — but they can buy you time. Many banks require evidence like pay stubs, layoff notices, or hospital records. It’s paperwork, yes, but it can prevent the spiral of late fees and damaged credit.

Loan Consolidation and Refinancing

If you’re juggling multiple loans, you have the right to explore consolidation. This combines your debts into a single monthly payment — ideally with a lower interest rate. You may also be able to refinance a high-cost loan for a cheaper one. Be cautious, though: these tools work best when your credit is still intact. If your score has already dropped, terms may not improve. Still, it’s worth checking.

Can You Walk Away? What About Default?

Voluntary Default Isn’t Simple

Some people ask: “Can I just stop paying and wait for it to go away?” Technically, yes — but the consequences are long-lasting. After 90+ days of missed payments, your loan is typically marked as in default. That means collections, court judgments, wage garnishment (in some countries), and years of bad credit. It’s rarely worth it unless you’re considering bankruptcy — and even then, legal advice is crucial.

Debt Settlement or Write-Off

In extreme cases, lenders may agree to settle the debt for less than what you owe. This is called debt settlement. It usually requires a lump sum payment and may damage your credit score, but not as badly as long-term non-payment. It’s a last resort, but it’s a right you can negotiate — especially if your lender believes they won’t recover the full amount through legal channels.

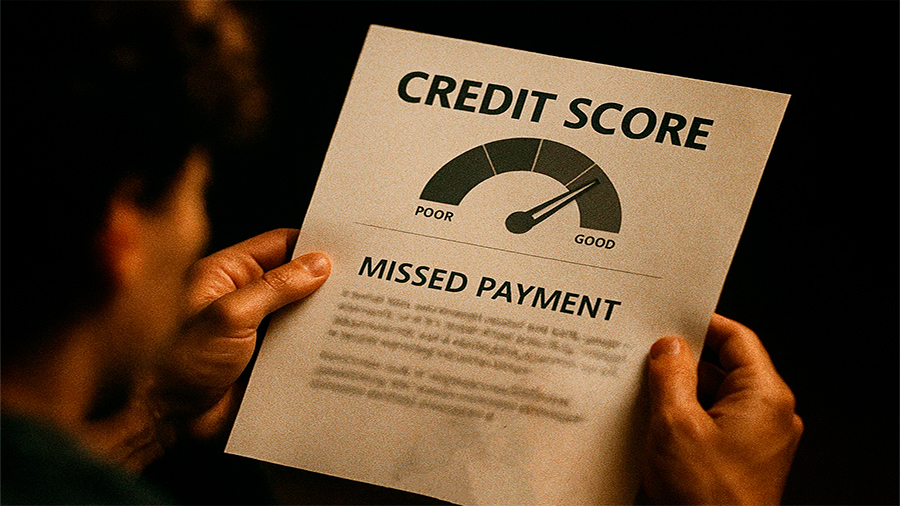

Your Credit Score: What Happens and What You Can Do

Missing a Payment Doesn’t Destroy Everything

A single late payment might not tank your score — especially if it’s corrected quickly. Most lenders don’t report delays until you’re more than 30 days overdue. If you’ve worked out a hardship plan, they might not report anything negative at all. You also have the right to request a note on your credit file explaining the reason behind a missed payment. This won’t erase it, but it adds valuable context for future lenders.

Dispute Inaccuracies

If your lender reports a late payment in error — or fails to note an approved deferral — you have the right to challenge it. Contact the credit bureau directly, provide supporting documents, and ask for a correction. Many reports contain mistakes, and cleaning them up is part of your financial recovery. You’re not stuck with incorrect records.

When to Get Outside Help

Free or Low-Cost Financial Counseling

Non-profits and government agencies offer credit counseling that can help you understand your rights and options. These aren’t shady debt settlement firms — they’re legitimate services that can contact lenders on your behalf and organize a formal repayment plan. Many people don’t realize this is available for free or at low cost.

Legal Aid Services

If you’re being sued or threatened with asset seizure, you may qualify for legal assistance. Depending on where you live, you might be able to get advice or even representation. Legal aid organizations often specialize in debt-related cases and can negotiate on your behalf or prevent lenders from overstepping.

The Conclusion: Don’t Wait Until It’s Too Late

Loan trouble doesn’t mean you’ve failed — it means you need a plan. And you have the right to ask for one. Lenders can’t ignore you. Laws are on your side. Your credit can recover. But none of that happens if you stay silent. As soon as repayment becomes a problem, act. Call your lender. Ask about options. Keep records. Know your legal protections. The earlier you move, the more control you keep. Because when it comes to loan issues, your greatest asset isn’t money — it’s action.