Loans Through Marketplaces: Convenient, But Is It Safe?

Online loan marketplaces are booming. They’re fast, easy to use, and promise more options than walking into a single bank branch. In just a few minutes, you can enter your personal info and get a list of loan offers from different lenders — with no pressure and no paperwork. For borrowers, it sounds ideal: choice, transparency, speed. But here’s the part most people miss — not every platform is built with your best interest in mind. Some expose your data, others push questionable lenders, and a few make money whether or not you get a loan you can afford. So yes, marketplaces are convenient — but they’re not always as safe as they seem.

What Makes a Loan Marketplace Different from a Lender?

When you borrow directly from a bank or credit union, you’re dealing with one institution. They evaluate your credit, set the rate, and fund the loan. With a loan marketplace, you’re dealing with a middleman. You fill out one form, and the marketplace forwards your information to a network of lenders. These lenders then respond with their own offers — and you get to choose.

This setup saves time. You don’t need to apply five different places to compare rates or approval chances. Instead, the marketplace acts as a filter and matchmaker. But the marketplace itself isn’t responsible for the loan you end up choosing. And that’s where things can get tricky. Once you click “apply,” you leave the marketplace — and enter the lender’s world. You’re now subject to their rules, their terms, and their customer service (or lack of it).

Why Loan Marketplaces Became So Popular

The traditional loan process can be slow. Going to a bank, sitting through a credit check, waiting days for approval — it doesn’t fit how people manage money today. Loan marketplaces solved that. They offer:

- Speed: Some approvals happen in minutes, with funding in 24–48 hours.

- Access: Even people with bad credit can find subprime or alternative lenders.

- Transparency: Side-by-side comparisons help borrowers make informed decisions.

- Control: You can browse offers without committing, and without a hard credit check (at first).

And for lenders, it’s equally efficient. Marketplaces provide pre-qualified leads — people already looking for loans. That makes customer acquisition cheaper and faster than traditional marketing. Everyone wins, right? Not always.

Where the Risks Start: Data and Privacy

Loan marketplaces collect a lot of sensitive information: income, employment, credit score, debt, even your Social Security number or national ID in some cases. That data is then sent to multiple lenders — and sometimes third-party marketing companies. Depending on the platform’s policy, your personal info might be used, stored, and shared in ways you didn’t expect.

If the site isn’t secure or doesn’t have clear privacy controls, you could receive spam offers, robocalls, or worse — your information could fall into the wrong hands. And because many marketplaces don’t directly underwrite loans, they may have less incentive to keep your data safe over time. You’re not their customer — you’re the product they sell to lenders.

Misleading Offers Are Common

Another red flag: not all marketplace offers are real. Some platforms advertise “as low as” interest rates that apply to only a tiny fraction of applicants. Others highlight pre-approval messages that vanish once you submit a full application. The most attractive terms often come with hidden conditions: higher origination fees, variable rates, early repayment penalties, or add-on insurance you didn’t ask for.

Even seemingly transparent marketplaces may use vague language like “estimated APR” or “average repayment,” which hides the actual cost. Some push offers from affiliated lenders first — even if better options exist elsewhere. The goal isn’t always to help you borrow smarter. Sometimes it’s just to get you to apply.

Unregulated Lenders Slip Through the Cracks

Reputable marketplaces screen their lending partners. They work only with licensed institutions and reject predatory lenders. But others don’t vet carefully — especially in countries where financial regulation is weak. That means you could be matched with high-interest payday lenders or installment companies that charge triple-digit APRs and aggressive late fees.

If you’re desperate — say, covering medical bills or urgent repairs — you might accept any loan that promises fast cash. But once the repayment terms kick in, the cost becomes overwhelming. And because you found the lender through a marketplace, it’s easy to assume it’s trustworthy when it’s not. The risk is higher when you’re in a rush.

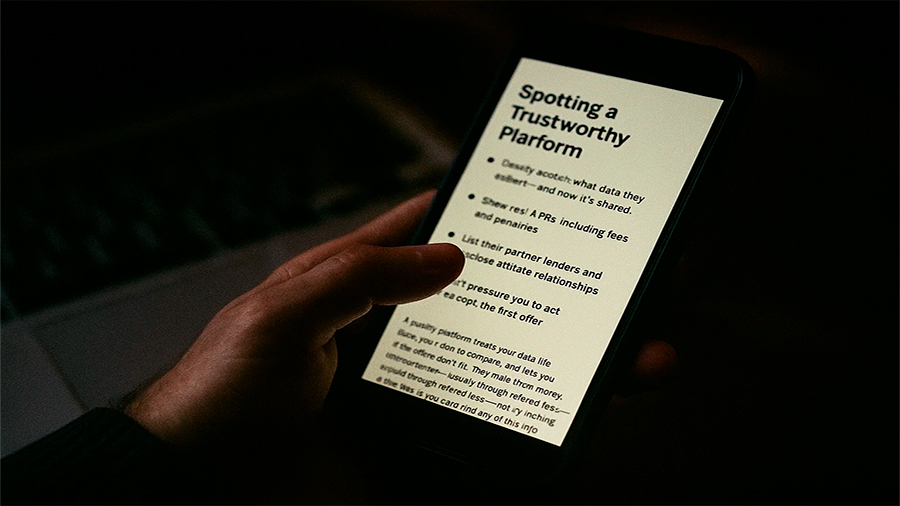

Spotting a Trustworthy Platform

How can you tell if a loan marketplace is legit? Start by checking if they:

- Clearly explain what data they collect — and how it’s shared

- Show real APRs, including fees and penalties

- List their partner lenders and disclose affiliate relationships

- Don’t pressure you to act immediately or accept the first offer

- Offer customer support and terms in plain language

A quality platform treats your data like it matters, gives you room to compare, and lets you walk away if the offers don’t fit. They make their money transparently — usually through referral fees — not by tricking you into a bad deal. If you can’t find any of this info, that’s a warning sign.

What to Do Before You Click “Apply”

Using a loan marketplace isn’t bad — in fact, it can be a helpful tool if used wisely. But before you submit your info, make sure:

- You’ve reviewed the platform’s privacy policy and data handling practices

- You know whether the credit check is soft or hard

- You understand the terms behind any “pre-approval”

- You’re ready to compare not just rates, but total cost of borrowing

After you get offers, don’t rush. Visit the lender’s website. Read customer reviews. Confirm licensing or registration. Ask questions if something feels off. And remember — it’s better to wait a few hours and get it right than to lock yourself into a 3-year loan that costs more than you expected.

The Conclusion

Loan marketplaces have changed the way we borrow. They’ve made the process faster, more open, and in some cases, more fair. But that doesn’t mean they’re risk-free. Behind the slick design and instant approvals are complex data flows, competing incentives, and lenders you might not know well. If you treat the platform like a search engine — not a guarantee — and take time to understand the real costs, you can benefit from the convenience without falling into traps. Like most tools in modern finance, it all comes down to how you use it.